Phil is great to work with and he has great customer service.

The owner is always available when we need him most…

WholePay is a friendly, personable company to do business with.

It is rare to find real integrity in this cut-throat industry.

Unless your processor has done all of the following, they approved your application, not your operation.

Reviewed each of your offers and terms.

Looked at your client agreements and refund language.

Reviewed your processing history and chargeback exposure.

Approved you for what your business actually does.

That gap between what you do and what they approved you for is where the risk lives.

Your processing agreement has terms that govern what happens when volume spikes, disputes come in, or something goes sideways. Here are a few that matter.

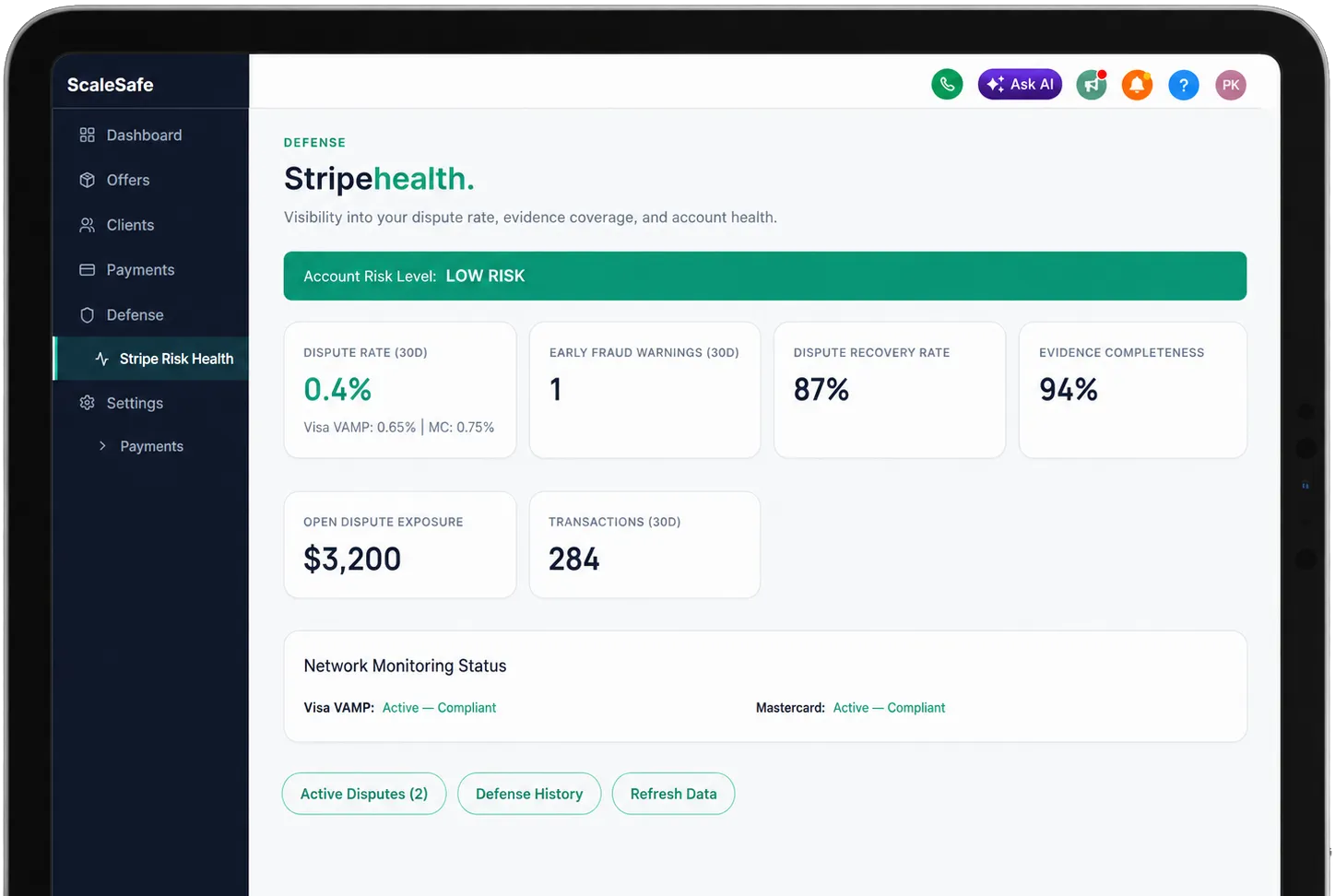

Two chargebacks out of 100 transactions puts you at a 2% ratio, well above the 1.5% threshold that triggers card brand monitoring programs.

Your processor sets expected volume parameters around your account. Step outside them and an automatic review is triggered.

Card brand policy has specific rules about income claims, guaranteed results, and how you describe outcomes.

If your refund policy conflicts with what the card brand considers reasonable for your transaction type, the bank sides with the cardholder.

The difference between being exposed and being prepared.

Your launch volume is coordinated with the bank before you go live.

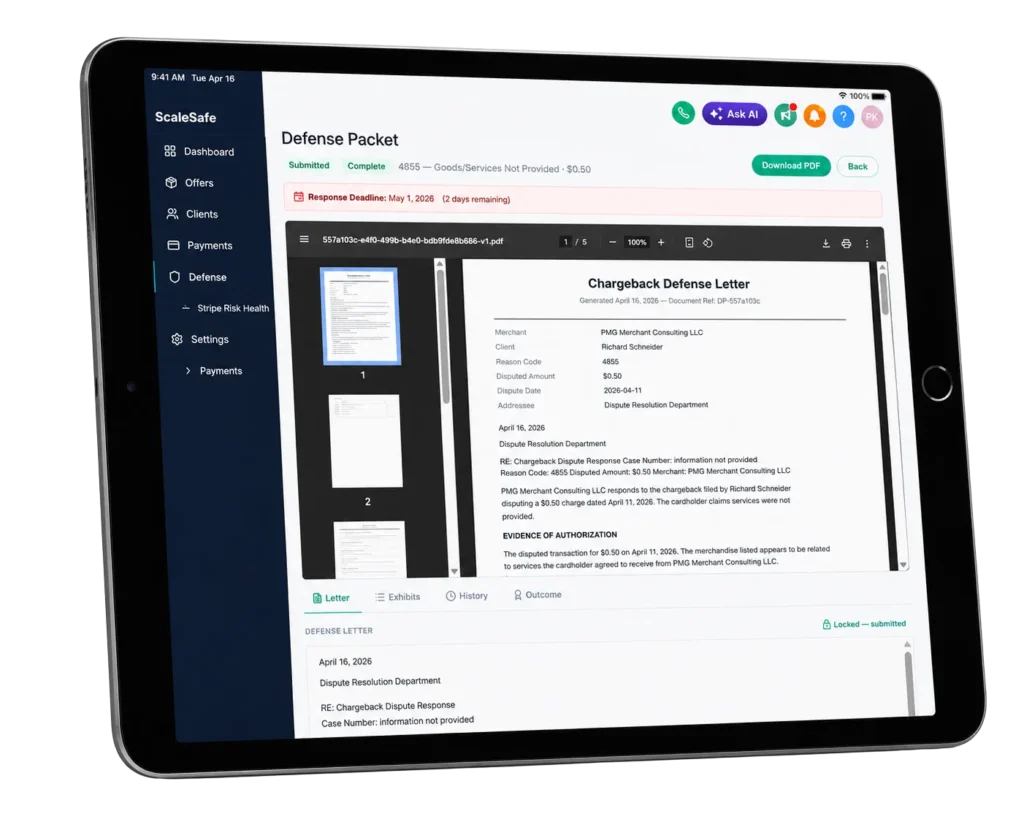

A dispute hits and you pull a complete evidence packet in minutes.

Your terms and your marketing hold up under review because they were built to.

Your chargeback ratio is monitored in real time.

When something goes wrong, your team talks to the underwriting team directly, presents the documentation, and makes the case for your business.

You receive a packet that shows you exactly where your business is exposed and copy-paste fixes for each gap. Offers, terms, refund policy, marketing claims, billing structure, processing history, and pricing are all reviewed against bank and card brand standards. Where your pricing can be optimized, we show you the math.

It is 100% free. No sales call. No pitch. No commitment.

We present your case to a bank that reviews your model and approves you specifically. Not a credit check. A real underwriting review by people who understand what you do and how you deliver it. Approvals typically come back in 24 to 48 hours after submission.

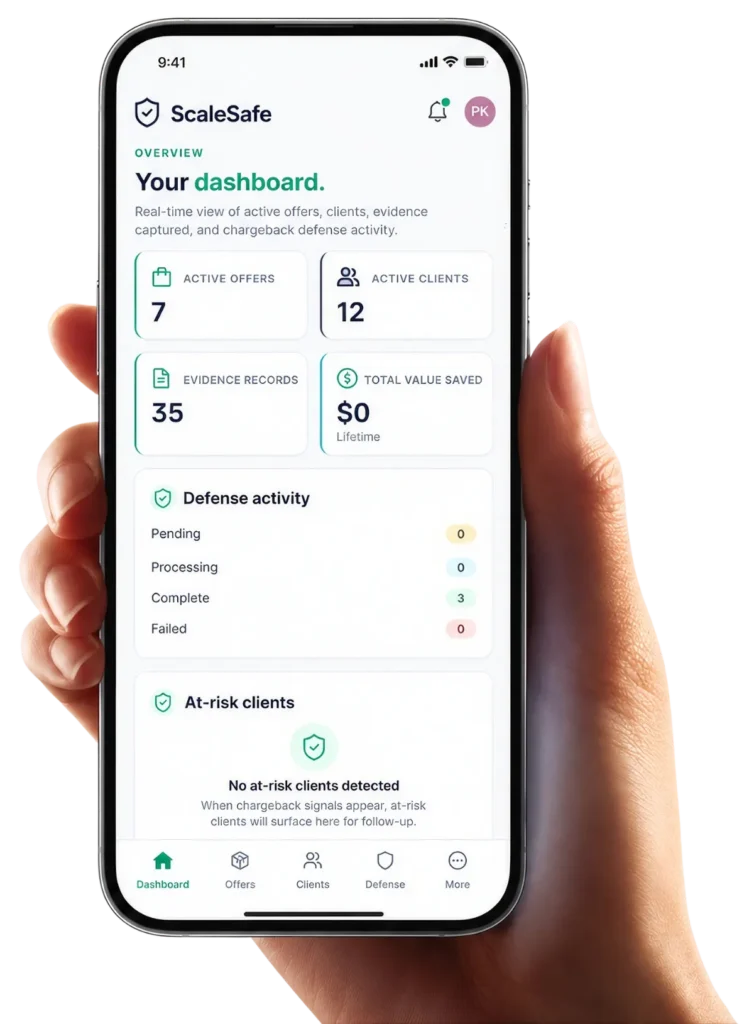

Every transaction tells a story. ScaleSafe makes sure you can prove yours.

Every client acknowledges your terms, refund policy, and deliverables before their card is charged. Timestamped and stored.

Session completions, milestone acknowledgments, communication touchpoints, resource access. Captured automatically inside the tools you already use.

When a chargeback comes in, ScaleSafe pulls your stored records and generates a complete evidence package formatted for the specific card brand and reason code.

ScaleSafe is not a guarantee against chargebacks. It is a system designed to reduce your exposure and respond with stronger evidence.

Three ways to process payments. One of them is yours.

Aggregators get you live in minutes. But they lack the infrastructure to support high-ticket professional service businesses where outcomes are subjective and delivery is digital. WholePay takes more time upfront. In exchange, you get infrastructure that matches the seriousness of what you have built.

Others sell processing access. WholePay helps you become a business the financial system can actually support.

Your clients are great. Your business model works. But the financial system was not built for what you do, and the one-off situations that come with high-ticket services can create real problems if your infrastructure is not ready for them. We help you tighten that infrastructure before those situations arrive.

You run high-ticket engagements where the outcomes are subjective and the delivery is digital. One disengaged client who files a chargeback instead of having a conversation can move your ratio above the threshold.

You take on larger clients with larger scopes, and every project comes with milestone decisions that can turn into disputes. One unhappy client can skip the conversation with you and go straight to their bank.

You sell access, community, and transformation, none of which come with a tracking number. One successful launch can trigger the same monitoring response as fraud if volume is not coordinated in advance.

Your clients pay large retainers before the work is complete. One advance payment can look like unaccounted risk to a bank that does not understand your timeline. Dedicated pages for each vertical with specific solutions.

Clients go where they are being served and our clients win because we serve them.

I know how the system works from the inside. From sitting in the rooms where pricing gets built, where risk policies get written, and where decisions about merchant accounts get made.

The system is not broken. It works exactly as designed. It is designed to move money and manage liability for the institutions involved. It was never designed to protect you. That is not a conspiracy. It is a business model.

The businesses driving this economy deserve infrastructure that matches the seriousness of what they have built. A real relationship with a real institution that has reviewed their business and approved it specifically. And someone on their side who knows how the system works, plays it on their behalf, and picks up the phone when it matters. That is what you get when you work with us.

You ask. We answer everything about high-ticket payment processing.

To the financial system, yes. What changes is whether that risk is managed intelligently or left unaddressed.

A free analysis of your payment infrastructure with specific findings and actionable fixes. No sales call. No commitment. Details in Step 1 above.

No. Your new merchant account deposits directly into your existing business bank account. You keep your current processor running until your new account is live and tested. There is no interruption to your business.

WholePay helps you become a business the financial system can actually support.